DIGITAL TRANSFORMATION IN BANKING

Dec. 21, 2023, 5:12 a.m.DIGITAL TRANSFORMATION IN BANKING

Use of Technology in the Banking Operations

Digitalisation of Banking

- We all know computerisation in Banking has led to Digitization of the sector

- In 1988 the RBI – set up a Computerisation Committee which was chaired by Dr. C Rangarajan.

The Quest for Excellence Continues

CORE - Centralized Online Real-time Exchange

- It is the ability of CBS to process Loans and Deposits (Assets & Liability) with interface to General Ledger system and reporting tools.

- Through this banks offer services across platform namely Branch banking ATM’s, Internet Banking Mobile banking to its customers.

What does the Core Banking Technology do

It is a service provided by a Bank through a connection of networked Branches through which the customer can access their bank accounts and perform basic transaction from any of the branch offices.

Digital Banking

Banking services delivered over the Internet is referred to as Digital Banking

- Providing more convenient and faster banking services

- Involves high level of process automation and

- Web based services may also include

- deploying of API – Application Programming Interface.

Regulators role in Digital Banking

Purpose?

To address competition arising from Opening of the economy in early 1990 – 1991 – 92 from private sector banks and Multinational banks.

Digital Banking does away with

Banks repetitive nature of

- the “Services” offered wrt “Processes”

- “Reduce errors” addressing the

- “Scale”

- “Geographical coverage” and to offer

- “Competitive Advantage”

What does the CBS technology do

- It reduces cost – Refer below Example

- Increases Agility

- Transforms operations

- Opens new channels for growth

- Data driven decisions

Digital Banking Products, Delivery Channels and Payment Systems

Types of e-Payment and Settlement Systems

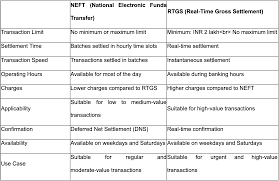

Gross Settlement System – RTGS

- Real Time Gross Settlement

- It is the fastest possible transfer mechanism for payments and settlements through the banking channel.

- Minimum value of transaction ₹2,00,000 and maximum. No Upper Limit on retail Internet portal.

- Customers can use the RTGS facility 24 hours on their internet banking

Net Settlement Systems - NEFT

National Electronic Fund Transfer

- It is used to transfer funds from one financial institution to other in India

- Transfer basis executed in hourly batch

- no minimum or maximum fund transfer limit

IMPS - Immediate Payment Services

Its builds a robust and cost effective real-time retail payment service available round-the-clock (also on holidays)

UPI – Unified Payment interface

Is a system that powers multiple bank accounts into a single mobile application (of any participating bank) merging several banking features, Seamless fund routing and merchant payment into

Payment Systems

NPCI- National Payment Corporation of India

- It is an initiative of the RBI and the IBA Under the provisions of the Payment and Settlement Systems Act, 2007. NPCI was set up for operating retail payments and settlement systems in India.

- The ten core promoter banks are SBI, PNB, Canara Bank, BOB, Union Bank of India, BOI, ICICI Bank, HDFC Bank, Citibank N. A. and HSBC.

- In 2016 the shareholding was broad-based to 56 member banks to include more banks representing all sectors.

- The NPCI started its role as a payment system provider by operating the ATM network when IDRBT handed over to it the National Financial Switch (NFS).

- Thereafter, the RBI requisitioned the NPCI to operate the Cheque Truncation System (CTS) on its behalf.

IMPS

An innovative real-time payment service that is available round-the-clock (even on holidays) and facilitates

- interbank (available with select PPIs also),

- Account to Account (or to wallets* also)

fund transfer

IMPS Benefits : True or False ?

- Domestic transfer within 2 hours

- Available 24 hours a day on all week days, entire year

- Fast, Inexpensive, and Safe

- Available mostly at BC Points and through Internet Banking

- Are Aadhaar No. based transaction enabled

- Whether non-financial services are also available

IMPS Benefits

- Real-time domestic fund transfer

- 24 X 7 X 365 availability

- Simple and easy to use

- Fast, Inexpensive, Safe and secure

- Channel Independent

- AADHAAR No. based transaction enabled

- Financial and non-financial service available

- Alternate input options

- Multiple access mechanism

Types of Remittances

- P2P

- Person to Person fund transfer

- Using Mobile number & MMID

- P2A

- Person to Account fund transfer

- Using Account number & IFS Code

- ABRS

- Aadhaar Based Remittance Service

- Using Aadhaar Number

- FIR

- Foreign Inward Remittance

IMPS- Customer Access Channels

- Self Service

- Mobile Application

- SMS

- Online: Net banking

- ATM

- Assisted Model

- BC Outlets, PPI Outlets

- Branches

UPI - UNIFIED PAYMENT INTERFACE

Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood. It also caters to the “Peer to Peer” collect request which can be scheduled and paid as per requirement and convenience

- Push and Pull Payments

- UPI ID (‘Username@PSPName’)

(No need to share Bank account details)

- Transfer using Single identifier like Virtual Address or Aadhaar No

- Banks – (Payment Service Provider) will provide App to customers of any bank

- One App for all transaction needs

- Single Click 2 Factor Authentication

BENEFITS OF UPI

To End User

▰ Privacy - Share only Virtual Address and no other sensitive information

▰ Multiple Utility - Cash on delivery/bill split sharing/ merchant payments / remittances

▰ One Click 2 FA - Authorize transaction by entering only the PIN

▰ Work across various interfaces - Payment request generated on Web interface; authorized on Mobile interface (App)

▰ Payment through Aadhaar Number - Pay using the Aadhaar number

▰ Availability & Security - Available 24*&*365. Customer does the transaction on his personal device

▰ Single click 2FA facility to the customer - seamless Pull

▰ In-App Payments (IAP)

To Merchant

▰ Seamless fund collection from customers - single identifiers

▰ No risk of storing customer’s virtual address like in Cards

▰ Tap customers not having credit/debit cards

▰ Suitable for e-Com & m-Com/

▰ Resolves the COD collection problem

To Bank

▰ Simple (Single click 2FA)

▰ Universal App for transactions

▰ Leverages existing Infrastructure

▰ Secure

▰ Payments basis Single/Unique Identifier

▰ Tap C2B segment & E-Com / M-Com

UPI - UNIFIED PAYMENT INTERFACE

Simple Enabling Steps for Customers

- Download UPI App from PlayStore

- Install the App on Phone

- Set App login

- Create a virtual address

- Add your bank address

- Set UPI PIN

- Start transacting using UPI

UPI-TRANSACTION TYPES

Financial

- Sending Money (P2P)

- Collecting(Request) Money (P2P)

- Merchant Payments

Non - Financial

- Mobile Banking Registration

- Check Balance

- Generate UPI Pin

- Change UPI Pin

UPI TRANSACTION FLOWS - P2P

Person Initiated Payment by using UPI App

- Person enters UPI PIN

- Request is remitted to Remitter PSP

- PSP transfers the request to UPI server at NPCI

- NPCI validates the mpin and send a success message to the Beneficiary PSP.

- PSP transmits the acknowledgement to NPCI

- NPCI confirms to the remitter bank.

- Remitter Bank transfers the money to the debit of remitter’s account and confirms to NPCI.

- NPCI confirms to the beneficiary Bank.

- Beneficiary Bank sends acknowledgement to NPCI.

Collect Transaction - 4 Party

- Person initiates a collect request

- Request is remitted to Beneficiary PSP

- PSP transfers the request to UPI server at NPCI

- NPCI send the request message to the Remitter PSP.

- Remitter enters UPI PIN to approve

- Remitter PSP transmits the acknowledgement to NPCI

- NPCI confirms to the remitter bank.

- Remitter Bank transfers the money to the debit of remitter’s account and confirms to NPCI.

- NPCI confirms to the beneficiary Bank.

- Beneficiary Bank sends acknowledgement to NPCI.

UPI-IMPORTANT POINTS TO REMEMBER

- User to register Mobile Number with the Bank.

- User to keep the beneficiary details handy.

- User to keep the UPI pin handy

- User to have sufficient Mobile Balance(applicable for prepaid connections)

Digital Adoption in India

Digital Lending

Digital lending is a platform where one can borrow within a short period of time. Digital Lending permits borrowers to apply for any consumer or business loan product from any internet-working device at any location. Consumer or Business loan products are credit cards, business loans, or mortgage. Through a digital lending platform, the process of loan sanctioning is just a click away.

Digital Lending Process

1. Borrower applies for Credit facility through Website / Mobile App

2. Information flows to Loan Origination System

3. Proof of Identification & Address verification

4. Financial, Employment details submission and Credit Scoring Analysis

5. Video PD for Underwriting

6. Loan approval

7. Video KYC

8. Loan agreement and E-Sign & Registration for E NACH ( ECS)

9. Disbursal

10. Servicing of Loan

11. Collection

Comments (0)